AFFORDING YOUR KIDS’ EDUCATION

Getting into college is your kids’ job. Paying for it is probably be yours. Student loans are an option. But your ‘assignment’ is to understand all the other sources of help available to you and your student.

COLLEGE PREP

As you welcome your little one into this world, college education seems like light years away. However, before you know it, they’ll be starting high school and you’ll be wondering where the time went. What you needn’t be wondering is how to pay for the education expenses ahead. With careful planning and a saving/borrowing strategy, you and your children will be ready to take on the college years… and beyond.

ABCs, 123s & 529s

If you can, the best college saving plan is to start when your child is a baby. Yes, a baby. Most states offer a 529 college savings plan, where you and family members can contribute a little money each month. It gets its name after “Section 529 “ from the Internal Revenue Code.

Some advantages of this type of savings plan are federal and state tax benefits, control over the account, and if you set up an automatic deposit, you can simply let the savings build in the background with no further effort on your part. Depending on how much you set aside per month, you could easily have a few thousand dollars saved up by the time your child is ready for college.

In addition to the 529, another route to consider is long term stock investments or a mutual fund. If you start this investment at age 1, you have 18 years to let this grow.

Are you still not sure if you should save this early? Consider this: It is less expensive to save for college than it is to borrow. While you are still setting money aside, if you are saving you will build interest, but if you borrow you will pay interest.

HIGH SCHOOL ASSIGNMENTS

When your child begins high school, it’s time to start putting some college planning in place. For the student this means serious buckling down on his/her grades. If your child can take advanced placement (AP) courses, they can count towards part of a college credit, which will automatically save you tuition costs. And excellent grades often earns scholarship money.

Now is a good time for you and your child to discuss their plans for the future. In their sophomore year you should begin preparing for the SATs and also start a search for scholarships. Looking for scholarships early allows for a more thorough search when you’re not under pressure to fill out paperwork in their senior year.

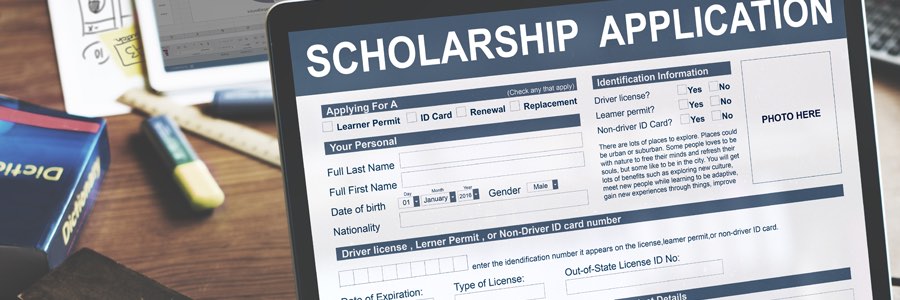

LOOK FOR “FREE” MONEY

Scholarships and grants are often called free money because you generally don’t have to pay the money back, unless you withdraw from the school. A good place to start the search for a scholarship is with the schools to which you are applying. Apply for every college scholarship you qualify for. Many college scholarships are left unawarded due to lack of applications. Leave no stone unturned in your search. Did you know that there are scholarships offered to left-handed people?

The Federal Pell Grants and The Federal Supplemental Education Opportunity Grants (FSEOG) assist undergraduates of low-income families, who are actively attending universities and or other secondary institutions. These types of grants are generally available only for students with “exceptional need.”

HELP FROM UNCLE SAM

There are a few steps to take when looking for federal aid from the government.

Get to know FAFSA (Free Application for Federal Student Aid). This is the first, but most important of many applications you’ll need to fill out for aid. You begin filling out the FAFSA in January of the year you’re applying to colleges, using the previous year’s tax return information.

Approximately three weeks after submitting the FAFSA, you and the schools you are applying to will receive a Student Aid Report (SAR). The SAR contains all the information you provided on your FAFSA. Schools use the SAR data to determine your eligibility for student aid.

Federal loans

Federal Direct Stafford Subsidized and Unsubsidized Loans are student loans that are guaranteed by the federal government, are applied for at the college, and are based on need. Students may qualify for a subsidized loan.

The Federal Perkins Loan Program provides low interest loans to help needy students finance the costs of post-secondary education.

The Parent Loan for Undergraduate Students (PLUS) provides fixed-rate education financing for parents of dependent undergraduate students. Parents cannot have an adverse credit history and students are required to fill out the FAFSA form first. PLUS loans can be used for tuition, fees, housing, books, supplies and more.

State grants

You know those property taxes homeowners like you have to pay every year? Consider state grants “payback time.” States use both property taxes and lottery funds to help fund student aid programs. Although most grants are given to students attending schools within the state, sometimes aid is available from your home state to use for out of state college tuition.

Once again, the process begins with the FAFSA (Free Application for Federal Student Aid) which calculates college costs and estimates your ability to pay. Even if you’re not eligible for federal aid, you might be eligible for financial aid from your state.

A word of advice: some state aid is awarded on a first-come, first-served basis. So be sure to know the deadlines, and submit applications early.

Contact your state grant agency for more information.

PRIVATE LOANS

Often times, federal loans and other financial aid are simply not enough to cover the full cost of college expenses. Supplemental loans are designed to help students who need additional assistance with educational costs. This student loan, also known as a privately insured loan, is different from federal loans because it has a variable interest rate. In most cases, it is advantageous for students to pursue a Federal Direct Unsubsidized Loan and for parents to pursue Federal PLUS Loans before seeking alternative loans.

The bottom line is this: Start early and save often. College is a huge expense that the majority of the population cannot pay on their own. Help is out there from federal, state and private levels. Do your homework on all of your options as early as you can.